Local Government Annual Budget Process: Step-By-Step Guide

It’s more important than ever to link your local government budget to your strategy.

Technically, a budget is simply a spending plan, forecasting the estimated revenue and expenses for a local government over a specified future period. But in reality, it’s so much more than that.

Good financial management is key to realizing an individual community’s vision, and the budget is among the primary tools guiding that pursuit. Not only does it help maintain financial accountability for local leaders, but it also represents plans for the future of the community at large.

With such a big job to do, it’s no wonder that the local government budget process is usually long and laborious. (But we don’t think it has to be, as you’ll soon see!) In this guide, we set out to explain an approach to budgeting that’s grounded in strategy, and which we believe delivers the best results. At the end, you can also read how one city has put this approach to work effectively to make its community a great place to live, work, and play.

Why A Local Government Budget Should Be Tied To Strategy

At its most basic level, the process of creating an annual budget is essentially planning for expected incomes and expenditures for the upcoming fiscal year. Naturally, that means allocating money across departments for purposes of both financing its operations and providing public services.

These needs often necessitate two different types of budgets:

- One is an operating budget, which is exactly what it sounds like—it lists expenditures necessary for day-to-day operations.

- The second is a capital budget, which includes financial plans for long-term capital improvements, facilities, and equipment. Both types of budgets play an important role in quality of life for residents.

For example, a city might need to budget annually for snow removal; it might also invest in a longer-term streetscape project that includes installing new and replacement sidewalks throughout the city.

Local governments that use both capital and operating budgets then consolidate them to indicate the amount of total estimated revenues available for the current period and the amount of new debt to be incurred for projects in the capital budget (which usually won’t generate revenue right away).

In general, governments have a good estimate of operating expenses from year to year because they are somewhat fixed costs. Most of the negotiating happens around the capital budget—which projects will you take on in the near future, and what will their impact be on the community?

To maximize your budget, it’s wise to choose projects that reflect your government’s stated future priorities, which you have outlined in your strategy and (presumably) communicated to your constituents.

Allocating financial resources to those projects that line up with your vision helps ensure you achieve those long-term priorities; it also promotes accountability and demonstrates good fiscal management. Your strategy also serves as a bridge between different departments, helping steer everyone toward common goals.

See how other local governments have successfully connected budget to strategy:

Learn how to link budget to strategy in our whitepaper

9 Steps For Conducting An Annual Budget Process That Links To Strategy

Following are the steps involved in the local government budget process, with a special focus on how to successfully link budget to strategy along the way. Note that this process could take up to eight months, so it begins well in advance of a new fiscal year.

Phase 1: Preparation (Takes Up To 6 Months)

1.Identify strategic objectives and gather department operating budget requests

Before a budget can be drafted, city managers need input from each department; that input comes in the form of budget requests. But before departments can submit their requests, they must be fully aware of the city’s strategic objectives, and identify related strategic objectives of their own. How will their activities best support the city’s strategic priorities? All budget requests should be linked in some manner to city-wide goals.

To formulate individual budget requests, department directors may gather input from their program managers. Once they are ready to be made, the requests themselves should be accompanied by contextual information that will be useful during the deliberation process, for example, revenue estimates, detailed expenditure lists, or program performance measures.

2. The chief executive holds meetings with department directors to review requests

Once department directors submit their budget requests, the chief executive begins the review process, holding meetings with department directors and budget staff to review the requests.

These discussions are usually held in the context of one of four types of budgeting approaches: priority-based budgeting, zero-based budgeting, budgeting for outcomes, and base budgeting. (For more information on each approach, check out this post.) Any of these approaches can link to your strategic plan; however, base budgeting—which also happens to be the most common form of budgeting, about 72% of surveyed local governments—may be the hardest to align with strategy because previously funded items continue to get funded. This makes it hard to drive change. Priority-based budgeting is the ideal if you want to make sure all funding dollars are working toward strategic goals.

3. Finalize the proposed budget and send it to the legislative body

After getting input from the department directors, the chief financial officer drafts a proposed budget, and reviews and negotiates it with department heads. Once this draft is complete, it is sent to the legislative body (e.g. city council, county council, or county board) for review.

Phase 2: Approval (Takes 1–2 months)

4. The legislative body reviews the budget in detail

Depending on the size of the legislative group, committees may oversee various parts of the budget. Each committee member reviews the budget in detail and makes revision suggestions as needed.

5. The legislative body may host a public budget hearing and information session for public input

Local government organizations are meant to service the public, so public input on the budget is crucial. Aside from hosting a public budget hearing and information session, they may also use other methods to gather public input, including citizen academies, discussion sessions, and surveys. It’s important, however, to consider public opinions in concert with objective data (like demographic information, for instance), expert knowledge (like that of engineers), and your strategic goals and priorities.

6. The legislative body approves the budget

After community input and review, the legislative body approves and adopts the budget.

Phase 3: Implementation & Evaluation

Takes place throughout the fiscal year for which the budget was created.

7. The budget office monitors expenditures

Once you create your budget and tie it to your priorities or outcomes, you still face the challenge of actually managing that budget (and your strategy along the way). Throughout the year, it’s important to monitor projected vs. actual spending and how departmental plans are progressing over time.

To do this, we recommend creating performance measures to help you determine if you’re accomplishing your strategic goals, clearly tying budget to performance. (Read more here about how one city department was able to validate its budget through performance management.) Data collection helps departments make budget decisions more effectively and holds everyone accountable for their actions. Remember to take the following steps:

- Assign an owner to every measure.

- Produce regular performance reports.

- Conduct regular meetings—monthly, quarterly, and annually—to ensure everyone stays on track.

- Periodically review your strategic plan to be sure the right goals are in place and the projects and measures continue to align with them.

8. At the end of year, the legislative body conducts a final budget reconciliation

This end-of-year reconciliation will reveal important information about how you actually used funds in relation to forecasted projections. (Note that some organizations do budget reconciliations on a quarterly basis to help guide spending, especially for departments that are spending ahead of their budgets. This allows them to bring their spending back inline before the end of the fiscal year.) You also want to ensure your records are accurate and complete.

This is also a good time to assess the performance of each department.

9. An independent auditor reviews the Comprehensive Annual Financial Report

Finally, an independent auditor ensures the budget complies with the annual financial report and follows accepted accounting principles.

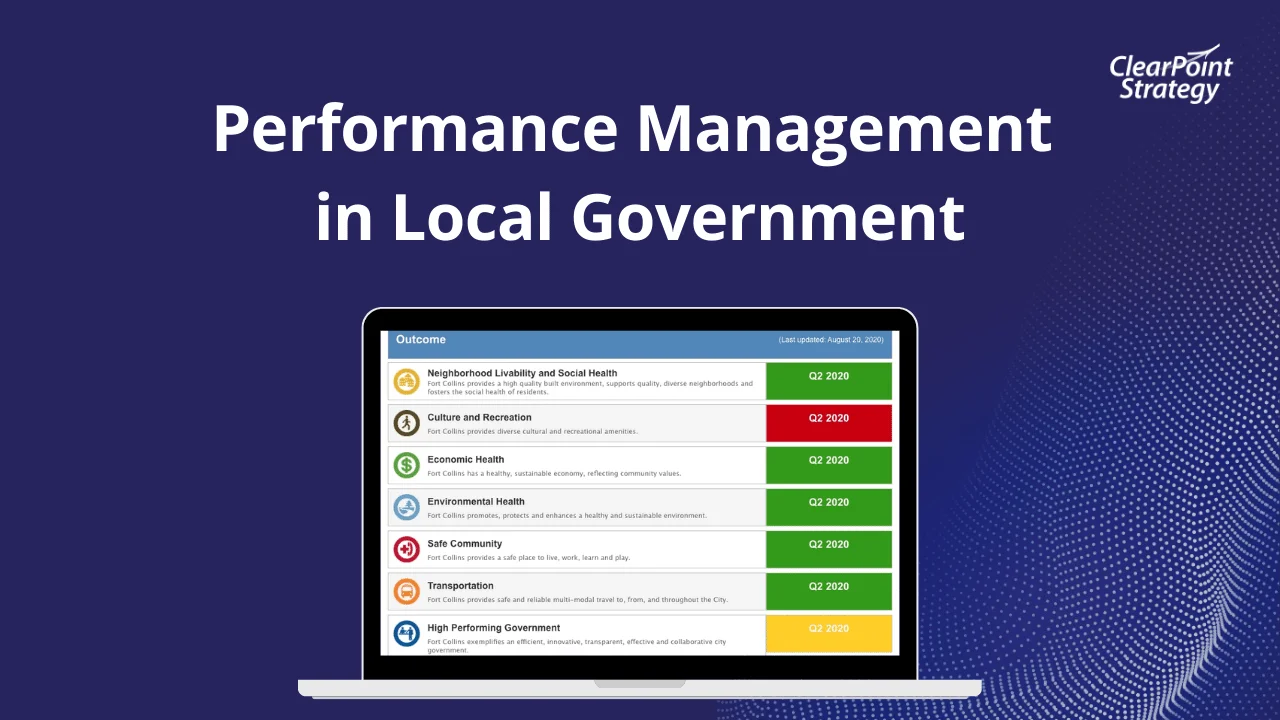

Fort Collins, CO: A Model for Budget-Strategy Linking

The city of Fort Collins, Colorado, provides a great exa,ple of how to link budget to strategy. Here are some of the highlights around this process:

- It all starts with the City's strategic plan, which considers input from residents, city council, and department heads. Every two years, the City takes the inputs it receives and creates a list of priorities within each of its seven strategic outcomes.

- Once the City Council formally adopts the City's proposed strategic plan, it kicks off the Budgeting for Outcomes process. Everything that is dunded in the budget must link back to the strategic plan, so initiatives that will help the City achieve its strategic objectives receive fundings.

- At the end of the year one of every two-year budget cycle, the City has the option to adjust the year two budget up or down as needed to balance the budget for the second half of the cycle.

- The city regularly checks in on the progress of its strategic plan, not only to assess the performance of linked metrics around its goals, but also the progress of linked programs and services funded in the budget. The City uses ClearPoint Strategy so it can easily see the linkages between funded initiatives and strategic objectives, as well as linked performance metrics.

- The City periodically hosts a City Council retreat to discuss issues facing the municipality and how it may allocate resources in the next budgeting cycle. This information is passed along to the steering committee. Then, at the beginning of the budgeting year, the steering committee presents the strategic plan to the council, who approves the plan so the city can budget accordingly.

Fort Collins' philosophy that linking budget to strategy would help it achieve strategic objectives has definitely paid off, allowing the City to better honor its commitments to the community.

See ClearPoint Strategy in action! Click here to watch a quick DEMO on the software

Align Your Local Government Budget with ClearPoint Strategy Sofware!

Creating an effective local government budget is about more than just forecasting revenue and expenses. Realizing your community's vision and maintaining financial accountability is also key. At ClearPoint Strategy, we provide the tools to streamline your budgeting process, ensuring it aligns with your strategic goals.

Ready to enhance your local government budget process? Book a demo with ClearPoint Strategy today and discover how our software can simplify the steps from preparation to evaluation.

Book your FREE 1-on-1 DEMO with ClearPoint Strategy